The Discipline of Building a Private Equity Allocation

By Chaya Slain, CFA, CAIA - President and CIO at Virtera Partners LLC

Since we launched Virtera, investors have asked how to find private equity opportunities and how much of their portfolios should be invested in private equity. Those are both important questions, but there is another question that matters just as much: how do you actually get the capital invested over time?

Many investors are familiar with the idea of making a commitment to a private equity fund, but they are less clear on what happens after that commitment is made. How quickly is the capital called? Why does the allocation take years to build? And why do investors need to keep making new commitments even after they reach their target allocation?

If investors do not understand the pacing, they can easily end up overcommitted, underinvested, concentrated in one vintage year, or surprised by the amount of time it takes to build the exposure they actually want.

Commitments Are Not Invested All at Once

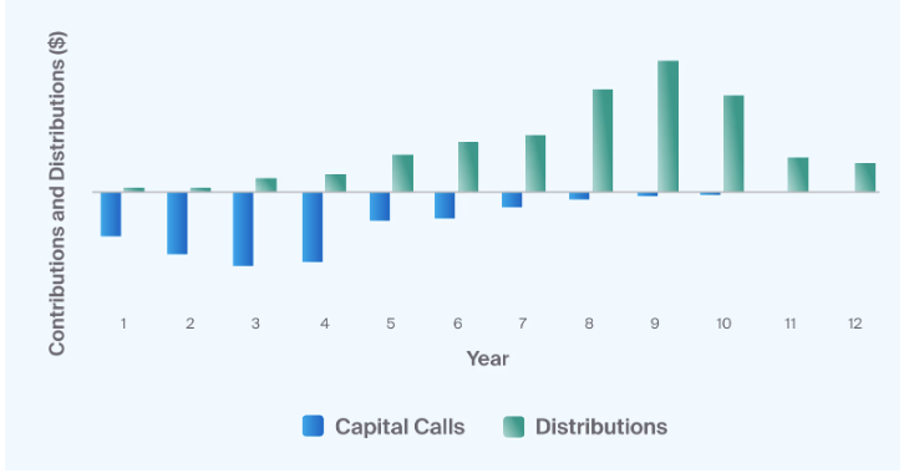

This is where private equity is very different from public markets. If you want public equity exposure, you can buy a stock, an ETF or a mutual fund. The decision and the deployment happen at the same time. With private equity, you make a commitment to a fund and the manager calls that capital over time as investments are made. This is the drawdown period and it generally takes three to five years. The investments are then typically held for another five to seven years before they are sold and the capital is returned to investors.

The chart below shows the cash flows from a typical private equity fund, although there can be wide variation from one fund to another. Most of the capital is called over the first several years and distributions usually begin in earnest around year five, with the bulk of the capital coming back in the later years of the fund's life.

Source: CAIS, Verus. For illustrative purposes only.

The chart does not represent any actual fund or any investment managed by Virtera. Actual capital calls and distributions vary significantly by fund and market environment, and there is no assurance that distributions will exceed contributions.

There are two practical issues investors need to understand. The first is that private equity exposure should not be concentrated in a single fund, company, strategy or vintage year. Just as dollar cost averaging can reduce timing risk in public markets, pacing your commitments over time can reduce timing risk in private equity. The goal is to build exposure across managers, strategies and market environments rather than concentrating it in a single moment.

The second is that, since capital comes back over time, you need to keep making new commitments to maintain the allocation. Investing in private equity is an ongoing program rather than a one-time decision.

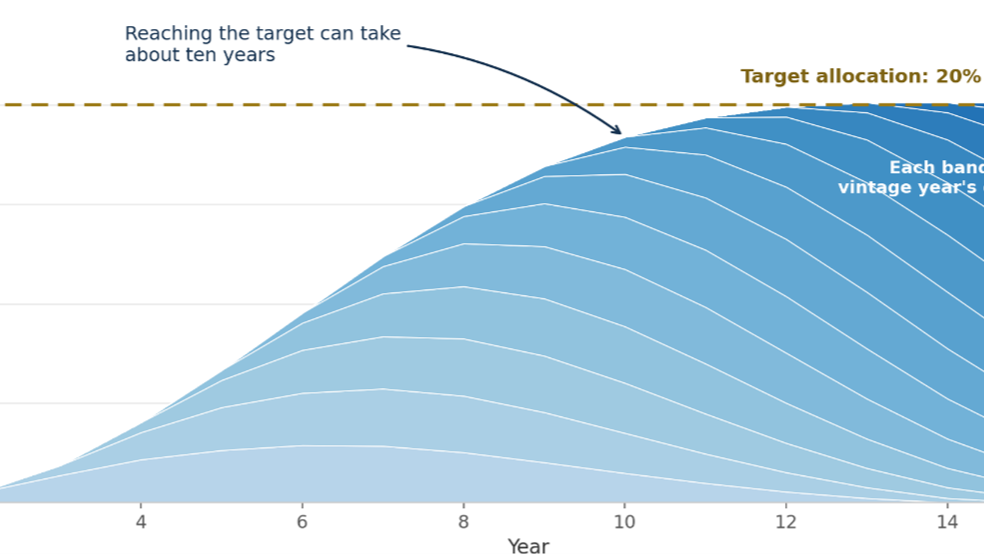

Getting to the Target Allocation Takes Years

Because capital is called gradually, it takes time to reach a target allocation. A good rule of thumb is to commit approximately 15% to 20% of your target allocation to private equity each year. This provides vintage year diversification and helps move a portfolio toward its long-term target.

For example, suppose an investor with a $25 million portfolio wants $5 million, or 20%, invested in private equity. That investor might commit roughly 3% to 4% of the portfolio each year, or $750,000 to $1 million annually.

The important principle is that cumulative commitments usually need to exceed the target allocation over time because only part of what you commit is invested at any given moment. Starting from no private equity exposure, it can take as long as ten years to reach a target allocation. Once a portfolio is mature, investors often find that a meaningful portion of the target is still represented by outstanding commitments made over the last few years and that capital calls can be funded, at least in part, by distributions from older funds.

At that point, the program can start to look more self-sustaining, although there is no assurance that distributions will be available to fund capital calls in any given period. Newer funds are still calling capital, but older funds are distributing capital back. The goal is not for the allocation to become perfectly stable but for the program to develop a more natural rhythm of capital going out and capital coming back.

This is not an exact science and these numbers are only rules of thumb. The pace of capital calls and distributions can speed up or slow down. Capital calls can accelerate when managers are finding more opportunities, while distributions can increase when exit markets are strong. They can also slow down when IPO markets are closed, M&A activity weakens or managers decide not to sell.

Diversification Matters

One of the main reasons to commit consistently is vintage year diversification. A vintage year is the year in which a fund begins investing and it matters because the market environment at that time can have a major impact on returns. The prices managers pay, the availability of financing, the level of competition and the exit environment all affect outcomes. Some vintage years will turn out better than others, but no one knows in advance which years those will be.

It is easy in hindsight to say that investors should have committed more in difficult markets and less in expensive ones, but it is much harder to do in real time. The years that feel most uncomfortable are often the ones when the best opportunities appear. The years that feel safest can be the most competitive.

The purpose of pacing is not to eliminate timing risk but to reduce the risk of making one large timing decision. By committing across multiple years, you participate in different market environments and the program does not depend on any single vintage.

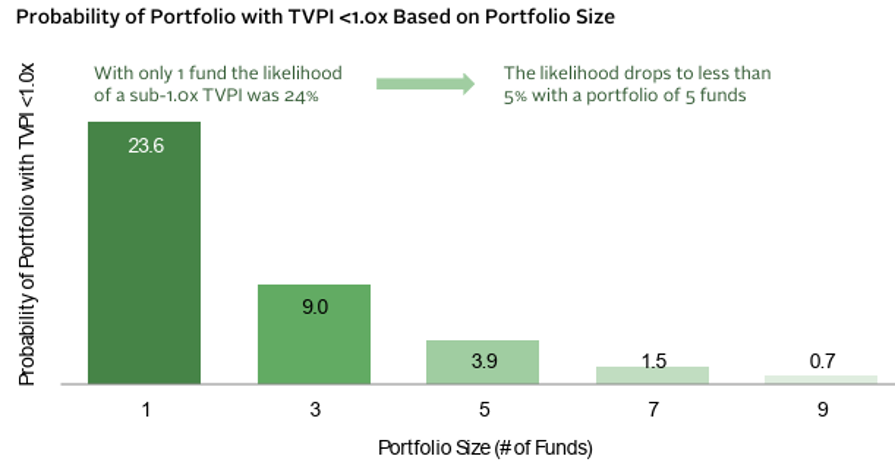

Manager diversification matters as well. The dispersion of returns across private equity managers is wide and the gap between a strong manager and a weak one can be large, which is why manager selection is so important. Cambridge Associates found that a portfolio holding a single fund had roughly a one in four chance of returning less than the capital invested, a risk that fell below 5% across a portfolio of five funds.¹

Source: Cambridge Associates (2018); see footnote 1.

Based on simulated portfolios constructed from historical benchmark data for funds formed between 1991 and 2005; results for more recent periods may differ. For illustrative purposes only. Not the performance of, or a prediction of the performance of, any Virtera client account or investment.

This is why most institutional private equity programs include multiple managers, strategies and vintage years, which reduces the risk that one poor manager, one weak strategy or one difficult vintage has an outsized impact on the whole portfolio.

Replicating that kind of diversification is difficult for most investors to do on their own, given the time, relationships and diligence it requires. Many build the program with the help of an advisor or a diversified vehicle that spreads a single commitment across managers, strategies and vintage years. That is much of what we do for clients and investors at Virtera.

Bottom Line

Private equity is not a trade but a long-term allocation that has to be built and maintained over time. Investors need to commit consistently, diversify across managers and vintage years, keep enough liquidity to meet capital calls and accept that the allocation will move around along the way.

¹ Cambridge Associates, "Private Investing for Private Investors: Life Can Be Better After 40(%)," 2018. The probabilities are based on simulated portfolios drawn from Cambridge Associates benchmark data for 3,077 funds formed between 1991 and 2005. Simulated results are hypothetical, do not reflect actual trading or the experience of any investor, and are subject to the limitations of the underlying data and methodology. Past performance is not indicative of future results.

Important Disclosures

This material is provided for informational and educational purposes only and does not constitute investment, legal or tax advice, a recommendation, or an offer to sell or a solicitation of an offer to buy any security or any interest in any fund or other investment vehicle. Any such offer or solicitation may be made only through definitive offering documents to investors meeting applicable eligibility requirements. Private equity investments are speculative, are illiquid and subject to long holding periods and restrictions on transfer, involve a high degree of risk including the possible loss of the entire amount invested, and bear management fees, performance-based compensation and other expenses that will reduce returns. The examples, allocation percentages and pacing figures presented are hypothetical illustrations only, are not based on any actual client account, and are not recommendations for any particular investor; individual circumstances vary, and investors should consult their own advisers. Diversification and commitment pacing do not ensure a profit or protect against loss. Certain information herein has been obtained from third-party sources believed to be reliable, but Virtera does not guarantee its accuracy or completeness. Past performance is not indicative of future results.